In the wake of the public health crisis caused by COVID-19 and the resulting economic hardships, Congress passed several pieces of legislation intended to help with the United States’ health and economic needs.

To help CPAs, Enrolled Agents, and tax professionals, we’ve gathered below the key details and provisions of the federal stimulus legislation passed in 2020 as a result of the pandemic.

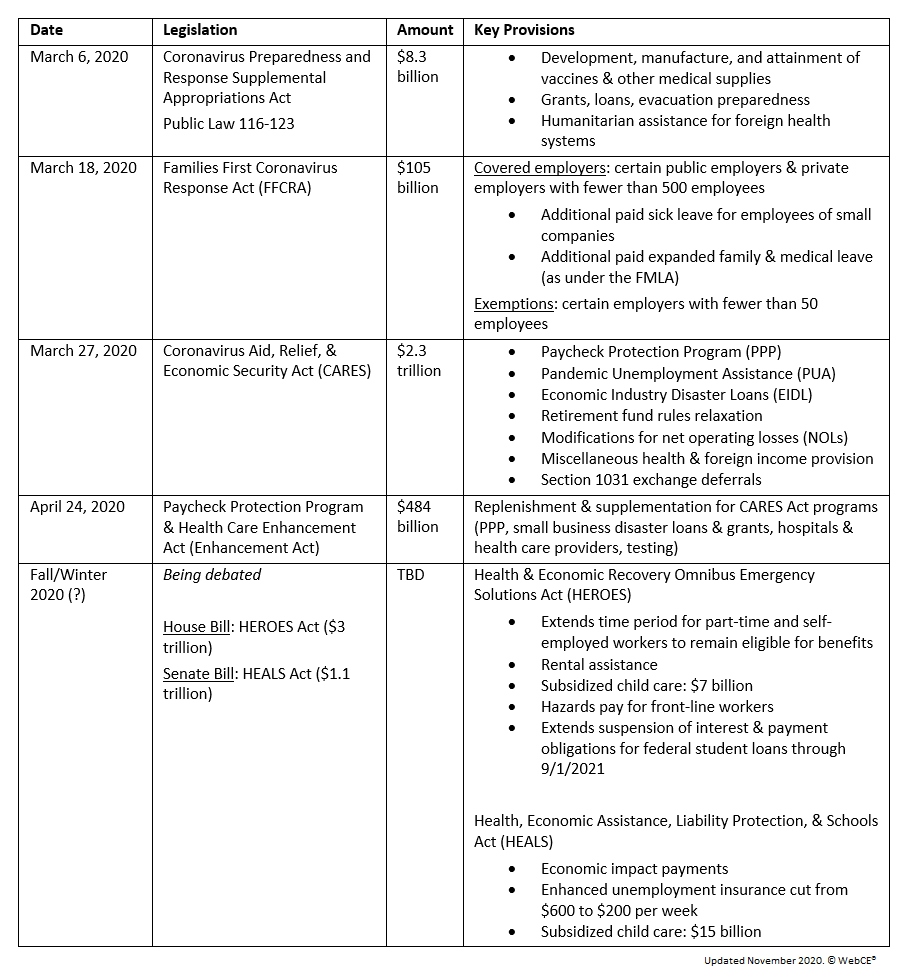

Coronavirus Preparedness and Response Supplemental Appropriations Act

The first stimulus law was passed on March 6, 2020, as the economic impact of the virus had just begun to noticeably disrupt the U.S. economy. The $8.3 billion in funds was directed primarily toward public health funding and vaccine development. Most funding was allocated domestically, with 19% being directed internationally to foreign public health systems.

Families First Coronavirus Response Act (FFCRA)

Next, the FFCRA (passed March 18, 2020) provided $105 billion in aid to cover extended sick leave and Family Medical Leave Act (FMLA) leave for people working for companies with fewer than 500 employees. Some federal employers or private employers with 50 or fewer employees were exempted from the requirement to provide such leave.

Additionally, Medicare and private health insurance plans were required to cover COVID-19 testing.

Coronavirus Aid, Relief, and Economic Security Act (CARES Act)

The largest stimulus package of the year, the CARES Act was passed on March 27, 2020. The law’s $2.3 trillion in aid comes in various forms of assistance ranging from paid leave to tax relief, detailed below.

Recovery Rebates

The Act authorizes, subject to adjusted gross income limitations, refundable tax credit payments of $1,200 for single filers and heads of household ($2,400 for joint filers) with $500 for each qualifying dependent child. These credits are not taxable and are not counted as income in determining a taxpayer’s eligibility for income-based programs such as Medicaid or health insurance Marketplace subsidies.

Paycheck Protection Program (PPP)

As part of the CARES Act, the Paycheck Protection Program provides eligible small businesses with no-collateral loans to pay for rent, utilities, mortgage interest, and up to eight weeks of payroll and benefits costs. Qualifying sole proprietors, independent contractors, and self-employed individuals are also eligible for these forgivable loans.

Loan forgiveness may generally be up to the full principal and accrued interest as long as the loan proceeds have been used for the indicated purposes.

When indebtedness is canceled under this program, the resulting imputed income is excluded from the borrower’s gross income.

Payroll Tax Deferral

The employer’s share of Social Security tax may be deferred, with half of the required amount due by December 31, 2021, and the other half by December 31, 2022. If the deferred amount is not repaid, the employer is solely liable for taxes and penalties. Further, an employer is not eligible for this deferral if it has had indebtedness forgiven under a PPP loan.

Pandemic Unemployment Assistance (PUA)

The PUA provisions of the CARES Act provide for federal unemployment benefits of $600 per week in addition to any state-provided unemployment assistance and extends the usual maximum period of unemployment benefits by 13 weeks for a total maximum period of 39 weeks. States are not permitted to reduce their unemployment benefits in amount or duration during this extended period.

DOL guidance indicates that employees are eligible for up to an additional 10 weeks of paid expanded family and medical leave at 2/3 the employee’s regular pay rate if that employee must care for a child whose school or child care provider is closed or unavailable for COVID-19 related reasons. Eligibility for benefits is far broader than under typical state unemployment laws. Self-employed persons and those with limited employment history are eligible for certain benefits provided under the CARES Act.

Individuals who may be otherwise able to and available for work but are unemployed, partially unemployed, or unable or unavailable to work because of the need to care for family or household members for COVID-19 related reasons. Additionally, primary caregivers for children or other household members may be eligible for PUA due to school or other facility closures.

Both regular unemployment insurance benefits and the unemployment insurance benefits expanded under the CARES Act are includible in gross income and subject to income taxes.

Employee Retention Credit

The Employee Retention Credit under the CARES Act encourages businesses to keep employees on their payroll. The refundable tax credit is 50 percent of up to $10,000 in wages and health plan expenses paid by an eligible employer whose business has been financially impacted by COVID-19. The credit covers payments made after March 12, 2020, and before January 1, 2021. The refundable credit is capped at $5,000 per employee and applies against certain employment taxes on wages paid to all employees.

Relaxation of Retirement Fund Tax Rules

The CARES Act provides for broader distribution options and favorable tax treatment for up to $100,000 in withdrawals, in aggregate, from retirement accounts (401(k), 403(b), and IRAs). This $100,000 limit is up from $50,000. The 10 percent early distribution penalty is waived.

Distributions may be included in income ratably over a three-year period unless the taxpayer elects to include the income in the year of distribution. IRA and qualified plan withdrawals may be rolled over within three years of distribution.

Charitable Contributions

The CARES Act temporarily allows an individual taxpayer to make tax-deductible cash contributions to qualified organizations of up to 100% (up from 60%) of AGI. Excess contributions may be carried forward for five years. For a non-itemizing taxpayer, the CARES Act permits an above-the-line deduction (a “universal deduction”) of up to $300 for charitable contributions made in taxable years beginning in 2020.

Corporate taxpayers also have larger limits and may also carry excess contributions forward.

Net Operating Losses

Under the Tax Cuts and Jobs Act (TCJA), net operating losses (NOLs) arising in taxable years ending after December 31, 2017, could not be carried back to reduce taxable income in prior years but could be carried forward indefinitely. The TCJA also limited the NOL deduction to 80 percent of taxable income.

The CARES Act temporarily provides for a five-year carryback for 2018 through 2020 losses and removes the 80 percent limitation. NOLs may still be carried forward indefinitely. Additionally, owners of pass-through businesses may disregard the prior $250,000/$500,000 limits to offset non-business income for years 2018 through 2020.

Medical Expenses

The CARES Act adds to the types of medical expenses treated as “qualified medical expenses” for tax-deductibility and for reimbursement from HSAs, FSAs, and Archer MSAs. Telehealth and remote care are added to services for which a taxpayer may receive first-dollar coverage without interfering with HDHP eligibility.

Foreign Earned Income

The exclusion from income for a portion of foreign earned income and housing costs depends in part on the duration of a person’s physical presence in a foreign country. Under Revenue Procedure 2020-27, the Section 911 exclusion will not be impacted by days spent away from a foreign country due to the COVID-19 pandemic.

Additional Provisions

The CARES act additionally provides the following COVID-19-related tax relief:

- Timing requirements for Section 1031 like-kind exchanges have been relaxed so that there is greater flexibility in accomplishing a tax-favored transaction.

- More business interest expense is deductible.

- Certain payments toward employees’ student loans are tax-favored for the employer and employee (there is no payroll tax for the employer; there is no income tax for the employee).

Paycheck Protection Program and Health Care Enhancement Act (Enhancement Act)

On April 24, 2020, Congress provided additional funds to continue to cover costs of the PPP, small business disaster loans and grants, aid to hospitals and health care providers, and testing costs.

Future Stimulus Legislation

As of November 2020, multiple stimulus bills were being fiercely debated in Congress. Currently the Senate has passed the HEALS Act ($1.1 trillion) while the House of Representatives has passed the larger HEROES Act ($3 trillion). Neither body has agreed to take up the other side’s bill, and negotiations for a potential compromise remain ongoing.

Federal COVID-19 Stimulus Legislation: 2020 Summary Table

To learn more about 2020’s federal stimulus legislation, you can purchase our course Federal Response to the Coronavirus Pandemic. This course provides a general review of the principal provisions of the CARES Act and of other federal tax-related stimulus legislation passed during 2020. CPAs, EAs, and tax advisors will learn how to apply the changes from the different legislations, as well as how to explain these changes to their clients.

CPA CPE Catalog

EA CPE Catalog

Tax CE Catalog